Truth-in-Credit Act

fourteen The intention of the fresh TILA are “to assure a meaningful revelation regarding borrowing from the bank terms so the individual should be able to evaluate more readily different borrowing terminology available to him and avoid the fresh not aware the means to access borrowing from the bank.” fifteen This new TILA means loan providers to disclose particular very first factual statements about your order therefore, the individual will be given the information expected “to compare the price of borrowing and come up with an informed told choice towards the accessibility credit.” sixteen The brand new TILA cannot apply to the following: borrowing from the bank transactions related to extensions of borrowing from the bank getting mostly organization, industrial or farming objectives; deals in ties otherwise products accounts because of the a brokerage-specialist entered towards Securities and you may Change Percentage; borrowing from the bank transactions, aside from those in and therefore a security desire try otherwise tend to getting received for the real-estate or even in individual property made use of as the primary dwelling or other than just personal studies money, in which the full matter funded exceeds $twenty-five,000; public utility functions managed from the a state; or loans made, insured, or secured pursuant to help you label IV of one’s Degree Work. 17

Requisite Disclosures

Your situation-in-Lending Work doesn’t need a collector to disclose all lending options to an individual; instead, the brand new collector must reveal merely recommendations connected to the fresh exchange under consideration.

Necessary disclosures include the money costs, the latest annual percentage rate, or other conditions and therefore require reasons according to the TILA including the “count funded,” the newest “total away from costs,” as well as the “overall income speed.” 18 From inside the transactions the spot where the consumer has got the directly to rescind, new creditor also needs to disclose one to right and supply the appropriate variations for the do it of that proper. 19

The latest loans fees is understood to be “the sum of all fees, payable in person otherwise ultimately because of the individual whom the financing is actually stretched, and you will imposed directly otherwise ultimately of the creditor since an instance for the expansion regarding credit.” 20 Within the finance charge may be the (1) attract, date speed differential, and you may people count payable around a place, write off, or other program out of most fees; (2) services otherwise holding fees; (3) loan fee, finder’s fee, otherwise similar charge; (4) payment getting an investigation otherwise credit report; and you may (5) advanced or any other charges for all the make certain otherwise insurance coverage protecting the fresh collector resistant to the buyer’s standard and other credit losings. 21

Along with the loans charges, the online payday loans Massachusetts brand new TILA means disclosure of annual percentage rate. 22 Typically, it is “a measure of the expense of borrowing and that need to be announced annually and the calculation of which is determined by fundamental transaction.” 23 This new law outlines particularly the annual percentage rate are become determined with respect to the form of deal, and you can delegates power to your Government Set aside Panel in order to issue using legislation. 24

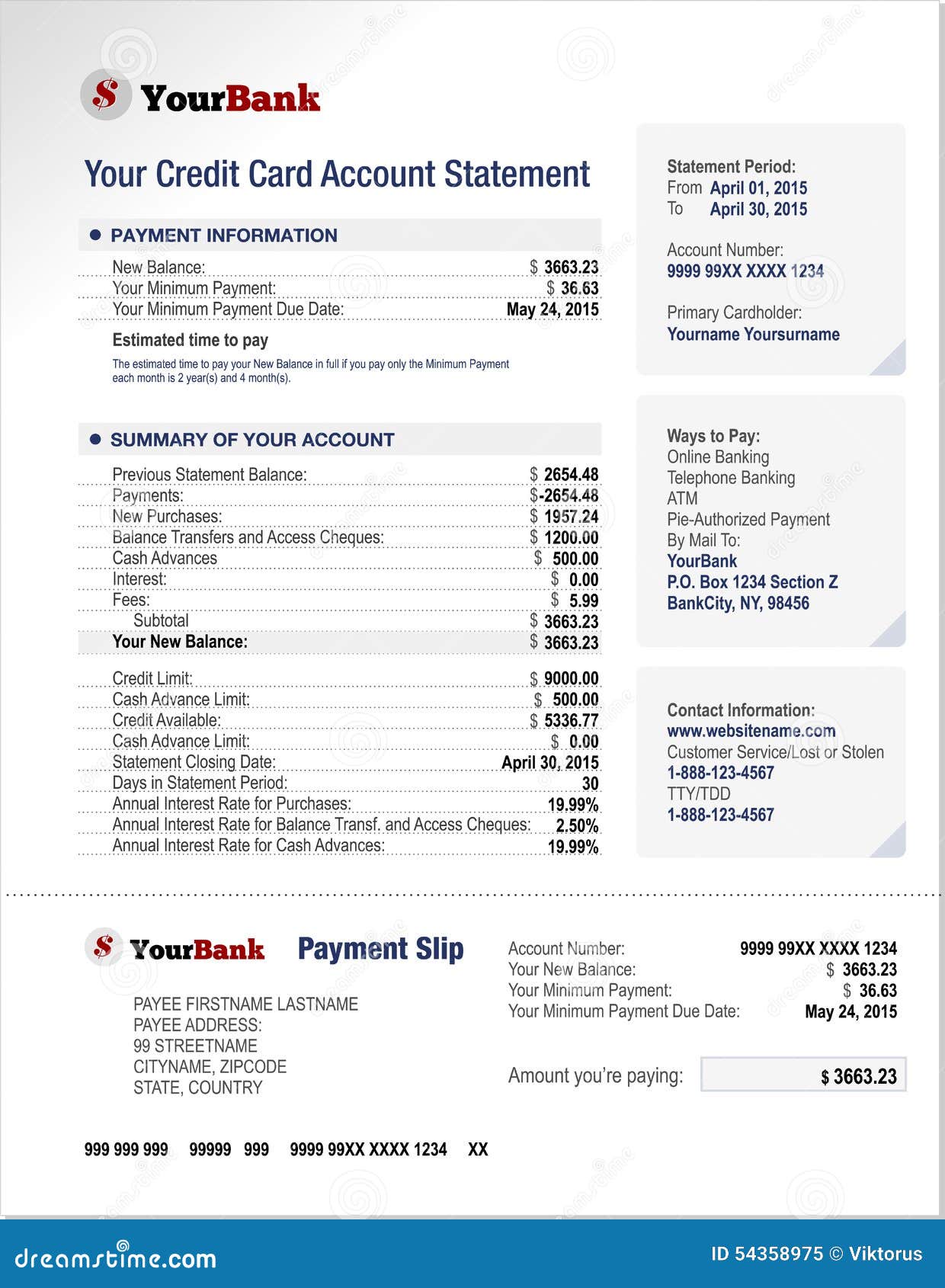

Before basic exchange is established, the fresh new collector have to furnish a first revelation, such as the loans fees, almost every other charges that can be imposed, the point that the collector have otherwise will and acquire a protection interest in the house bought, a statement away from charging rights, and you may household security information if appropriate. twenty-five New creditor also needs to furnish a periodic statement for every recharging duration at the conclusion of that the account has actually a debit otherwise borrowing from the bank balance of greater than $step 1 otherwise on what a finance costs might have been imposed. twenty six The occasional report have to be brought at least 2 weeks ahead of the stop of your battery charging years. twenty-seven Disclosures required in this new unexpected statement through the earlier equilibrium, an identification off deals, credits, periodic rates, the amount of the balance that this new unexpected speed was used, the amount of loans charge, brand new apr, most other costs, closure go out of your own battery charging period and you can this new harmony, the fresh 100 % free-trip several months, and target for see off battery charging mistakes. 28